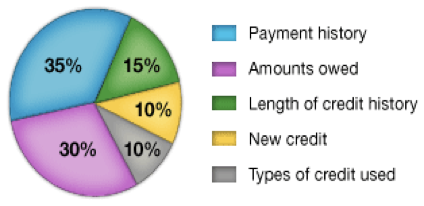

A Basic Guide to Understanding the Structure of Your FICO Score

These FICO Score percentages are based on the importance of the five categories for the general population. For particular groups-for example, people who have not been using credit long—the relative importance of these categories may be different.

Payment History

The first thing any lender would want to know is whether you have paid past credit accounts on time. This is also one of the most important factors in a FICO score. Late payments are not an automatic “score killer.” An overall good credit picture can outweigh one or two instances of, say, late credit card payments. But having no late payments on your credit report doesn’t mean you will get a “perfect score.” Your FICO score takes into account:

Payment information on many types of accounts.

These will include credit cards (such as Visa, MasterCard, American Express, and Discover), retail accounts (credit from stores where you do business, such as department store credit cards), installment loans (loans where you make regular payments, such as car loans), finance company accounts and mortgage loans.

Public record and collection items—reports of events such as bankruptcies, foreclosures, suits, wage attachments, liens, and judgments.

These are considered quite serious, although older items and items with small amounts will count less than more recent items or those with larger amounts. Bankruptcies will stay on your credit report for 7–10 years, depending on the type.

Details on late or missed payments (“delinquencies”), public records, and collection items.

The FICO score considers how late they were, how much was owed, how recently they occurred and how many there are. A 60-day late payment is not as significant as a 90-day late payment, in and of itself. But timing and frequency count, too. A 60-day late payment made just a month ago will affect a score more than a 90-day late payment from five years ago.

How many accounts show no late payments?

A good track record on most of your credit accounts will increase your FICO score.

Amounts Owed

Having credit accounts and owing money on them does not necessarily mean you are a high-risk borrower with a low FICO score. However, when a high percentage of a person’s available credit has already been used, this can indicate that a person is overextended, and is more likely to make some payments late or not at all. Your FICO score takes into account:

The amount owed on all accounts.

Note that even if you pay off your credit cards in full every month, your credit report may show a balance on those cards. The total balance on your last statement is generally the amount that will show in your credit report.

The amount owed on all accounts, and on different types of accounts.

In addition to the overall amount you owe, your FICO score considers the amount you owe on specific types of accounts, such as credit cards and installment loans.

Whether you are showing a balance on certain types of accounts.

In some cases, having a very small balance without missing a payment shows that you have managed credit responsibly, and may be slightly better than carrying no balance at all. On the other hand, closing unused credit accounts that show zero balances and that are in good standing will not raise your FICO score.

How many accounts have balances?

A large number can indicate a higher risk of over-extension.

How much of the total credit line is being used on credit cards and other revolving credit” accounts?

Someone closer to “maxing out” on many credit cards may have trouble making payments in the future.

How much of an installment loan account is still owed, compared with the original loan amounts?

For example, if you borrowed $10,000 to buy a car and you have paid back $2,000, you owe (with interest) more than 80% of the original loan. Paying down installment loans is a good sign that you are able and willing to manage and repay debt.

Length of Credit History

In general, a more extended credit history will increase your FICO score. However, even people who have not been using credit for very long may get high FICO scores, depending on how the rest of the credit report looks. Your FICO score takes into account:

How long have your credit accounts been established?

Your FICO score considers the age of your oldest account, the age of your newest account, and the average age of all your accounts.

How long it has been since you used certain accounts?

Types of Credit in Use

The score will consider your mix of credit cards, retail accounts, installment loans, finance company accounts, and mortgage loans. It is not necessary to have one of each, and it is not a good idea to open credit accounts you don’t intend to use. The credit mix usually won’t be a key factor in determining your FICO score—but it will be more important if your credit report does not have a lot of other information on which to base a score. Your FICO score takes into account:

The kinds of credit accounts you have.

Do you have experience with both revolving and installment-type accounts, or has your credit experience been limited to only one type?

How many of each?

Your FICO score also looks at the total number of accounts you have. For different credit profiles, how many is too many will vary depending on your overall credit picture.

New Credit

People tend to have more credit today and to shop for credit—via the internet and other channels—more frequently than ever. FICO scores reflect this reality. However, research shows that opening several credit accounts in a short period of time does represent greater risk—especially for people who do not have a long-established credit history. Multiple credit requests also represent greater credit risk. However, FICO scores do a good job of distinguishing between searches for many new credit accounts and rate shopping for the best mortgage or auto loan. Your FICO score takes into account:

The number of new accounts you have.

Your FICO score looks at how many new accounts you have by type of account (for example, how many newly opened credit cards you have).

How long it has been since you opened a new account?

Your FICO score may consider this information for specific types of accounts.

How many recent requests for credit you have made, as indicated by inquiries to the credit reporting agencies?

Inquiries remain on your credit report for two years, although FICO scores only consider inquiries from the last 12 months. FICO scores have been carefully designed to count only those inquiries that truly impact credit risk.

The length of time since credit report inquiries were made by lenders. Whether you have a good recent credit history, following past payment problems.

Re-establishing credit and making payments on time after a period of late payment behavior will help to raise a FICO score over time.